Foreclosures rose slightly from July 2021 in about two-thirds of metro areas, but the national rate remains near an all-time low

IRVINE, Calif. — (BUSINESS WIRE) — September 29, 2022 — CoreLogic, a leading global property information, analytics and data-enabled solutions provider, today released its monthly Loan Performance Insights Report for July 2022.

This press release features multimedia. View the full release here: https://www.businesswire.com/news/home/20220929005181/en/

Figure 1: National Overview of Loan Performance (Graphic: Business Wire)

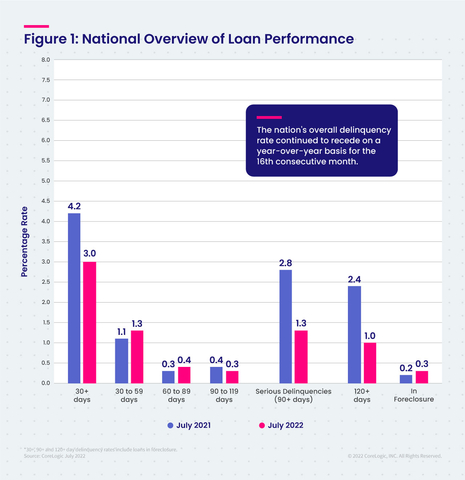

For the month of July, 3% of all mortgages in the U.S. were in some stage of delinquency (30 days or more past due, including those in foreclosure), representing a 1.2 percentage point decrease compared to 4.2% in July 2021.

To gain a complete view of the mortgage market and loan performance health, CoreLogic examines all stages of delinquency. In July 2022, the U.S. delinquency and transition rates, and their year-over-year changes, were as follows:

- Early-Stage Delinquencies (30 to 59 days past due): 1.3%, up from 1.1% in July 2021.

- Adverse Delinquency (60 to 89 days past due): 0.4%, up from 0.3% in July 2021.

- Serious Delinquency (90 days or more past due, including loans in foreclosure): 1.3%, down from 2.8% in July 2021 and a high of 4.3% in August 2020.

- Foreclosure Inventory Rate (the share of mortgages in some stage of the foreclosure process): 0.3%, up from 0.2% in July 2021.

- Transition Rate (the share of mortgages that transitioned from current to 30 days past due): 0.7%, up from 0.6% in July 2021.

Although overall U.S. mortgage delinquencies crept up again in July from earlier in 2022, they declined for the 16th straight month year over year and remained near historic lows. The national foreclosure rate has held steady at 0.3% since March but rose by 0.1 percentage point from July 2021. This slight bump mirrors metro-level trends, with almost two-thirds of areas that CoreLogic tracks posting small annual foreclosure gains. The minor uptick in foreclosures may be due to mortgage forbearance periods and moratoriums ending for some homeowners, while the increase in delinquencies could indicate that inflation is negatively impacting others’ abilities to make monthly payments.

“Early-stage delinquencies are showing a small but clear increasing trend on a month-over-month and year-over-year basis,” said Molly Boesel, principal economist at CoreLogic. “While the share of mortgages that are 30 to 89 days past due remains below the pre-pandemic level, the slight increase is occurring in most areas of the country and could indicate that more borrowers are having trouble making their monthly payments.”

State and Metro Takeaways:

- In July, all states posted annual declines in their overall delinquency rates. The states with the largest declines were Hawaii and Nevada (both down 2.3 percentage points), New Jersey (down 2.1 percentage points) and New York (down 2.0 percentage points), the third consecutive month that these states have led the country for delinquency declines. The remaining states, including the District of Columbia, registered annual delinquency rate drops between 1.9 percentage points and 0.2 percentage points.

- All but eight U.S. metro areas posted at least a small annual decrease in overall delinquency rates, with increases in those metros ranging from 0.1 percentage points to 0.4 percentage points.

- All U.S. metro areas posted at least a small annual decrease in serious delinquency rates, with Odessa, Texas (down 4.7 percentage points), Laredo, Texas (down 3.7 percentage points) and Kahului-Wailuku-Lahaina, Hawaii (down 3.6 percentage points) posting the largest decreases.

The next CoreLogic Loan Performance Insights Report will be released on October 27, 2022, featuring data for August 2022. For ongoing housing trends and data, visit the CoreLogic Intelligence Blog: www.corelogic.com/intelligence.

Methodology

The data in The CoreLogic LPI report represents foreclosure and delinquency activity reported through July 2022. The data in this report accounts for only first liens against a property and does not include secondary liens. The delinquency, transition and foreclosure rates are measured only against homes that have an outstanding mortgage. Homes without mortgage liens are not subject to foreclosure and are, therefore, excluded from the analysis. CoreLogic has approximately 75% coverage of U.S. foreclosure data.

Source: CoreLogic

The data provided is for use only by the primary recipient or the primary recipient's publication or broadcast. This data may not be re-sold, republished or licensed to any other source, including publications and sources owned by the primary recipient's parent company without prior written permission from CoreLogic. Any CoreLogic data used for publication or broadcast, in whole or in part, must be sourced as coming from CoreLogic, a data and analytics company. For use with broadcast or web content, the citation must directly accompany first reference of the data. If the data is illustrated with maps, charts, graphs or other visual elements, the CoreLogic logo must be included on screen or website. For questions, analysis or interpretation of the data, contact Robin Wachner at newsmedia@corelogic.com. For sales inquiries, contact sales@corelogic.com. Data provided may not be modified without the prior written permission of CoreLogic. Do not use the data in any unlawful manner. This data is compiled from public records, contributory databases and proprietary analytics, and its accuracy is dependent upon these sources.

About CoreLogic

CoreLogic is a leading global property information, analytics and data-enabled solutions provider. The company's combined data from public, contributory and proprietary sources includes over 4.5 billion records spanning more than 50 years, providing detailed coverage of property, mortgages and other encumbrances, consumer credit, tenancy, location, hazard risk and related performance information. The markets CoreLogic serves include real estate and mortgage finance, insurance, capital markets, and the public sector. CoreLogic delivers value to clients through unique data, analytics, workflow technology, advisory and managed services. Clients rely on CoreLogic to help identify and manage growth opportunities, improve performance and mitigate risk. Headquartered in Irvine, Calif., CoreLogic operates in North America, Western Europe and Asia Pacific. For more information, please visit www.corelogic.com.

CORELOGIC and the CoreLogic logo are trademarks of CoreLogic, Inc. and/or its subsidiaries. All other trademarks are the property of their respective owners.

View source version on businesswire.com: https://www.businesswire.com/news/home/20220929005181/en/

Contact:

Robin Wachner

CoreLogic

newsmedia@corelogic.com

Animation, 3D Art and 3D Models")